Delayed Financing: What It Is and How It Can Benefit Investors and Homebuyers in General

When purchasing a home, speed can be king in competitive markets like The San Francisco Bay Area, and Cash is King when writing offers! One strategy that’s growing in popularity among savvy buyers is delayed financing. Whether you’re a real estate investor or a homebuyer seeking more flexibility, understanding delayed financing can open up new opportunities for you.

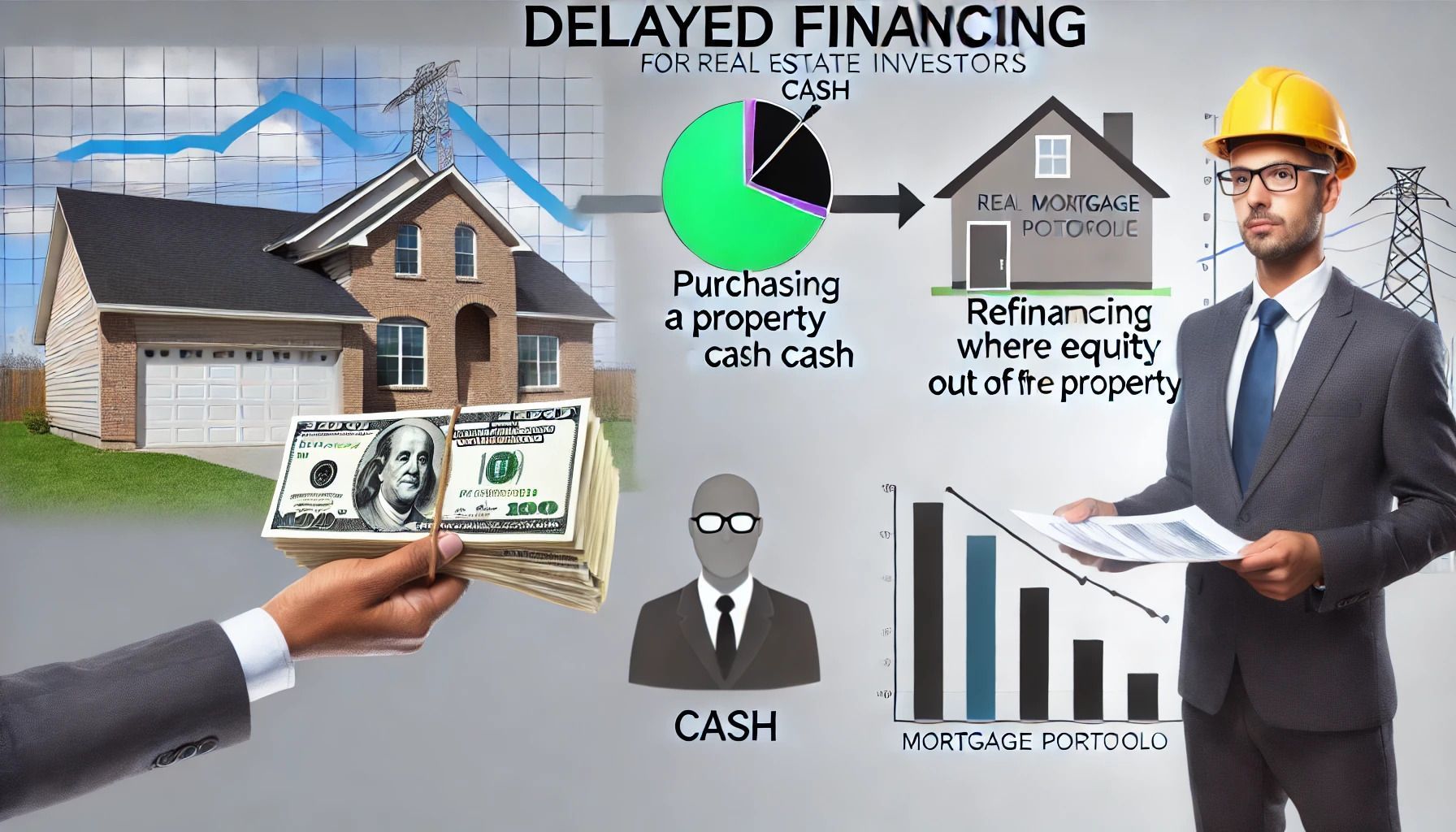

What is Delayed Financing?

Delayed financing allows a buyer to purchase a home with cash and then quickly refinance to recoup their investment. Fannie Mae and Fredie Mac currently have a 6-month seasoning period before they allow a homeowner to take out cash. Essentially, after buying a property outright, you apply for a mortgage after the fact, converting your equity back into liquid cash. The ability to refinance right after purchase—without the typical six-month waiting period—makes this option appealing, especially in competitive markets.

This financing tool is ideal for buyers who can make a cash offer to close the deal faster but don’t want to leave all their money tied up in the property. It’s most often used by investors or high-net-worth individuals but can also be a valuable tool for anyone in a position to pay cash up front and then restructure the purchase later.

How Does Delayed Financing Work?

Here’s how delayed financing typically works:

- Purchase the Home with Cash: Initially, the buyer pays for the property in full, without taking out a loan. Cash offers are especially attractive to sellers because they’re quicker to close and don’t rely on the buyer getting loan approval.

- Apply for a Cash-Out Refinance: After the purchase is complete, the buyer applies for a cash-out refinance to recover the cash used to buy the home. This can be done almost immediately after closing. The buyer refinances for the same amount or up to 75% of the home’s appraised value (depending on lender guidelines).

- Return to Regular Mortgage Payments: After the refinance is approved, the buyer receives a new loan and can use the proceeds to replenish their funds or invest in other properties. From this point on, the homeowner makes regular mortgage payments just like they would with a traditional loan.

Key Benefits of Delayed Financing

- Fast Close on a Home: One of the biggest advantages of using delayed financing is the ability to make a cash offer. In competitive markets, cash buyers are often preferred by sellers because they can close quickly, without the uncertainty of loan approval or delays in the mortgage process.

- Replenish Your Cash: Cash buyers can avoid tying up all of their liquidity in a single asset. By refinancing immediately after purchasing, they can regain access to their funds while still holding onto the property. This flexibility allows for new investments or addressing other financial needs.

- Avoid Waiting Periods: Traditional cash-out refinances typically require a six-month waiting period. Delayed financing bypasses this requirement, allowing buyers to refinance as soon as they need to. This speed is especially helpful for those who need immediate access to their capital.

- Tax Deductibility: In some cases, mortgage interest from delayed financing can be tax-deductible, similar to a traditional mortgage. Be sure to consult with a tax professional to understand your specific situation.

- Leverage Other Assets: Delayed financing allows buyers to use their cash when needed and then turn around and leverage their home like any other asset. This makes it an attractive tool for investors looking to maximize their buying power and portfolio growth.

Things to Keep in Mind

- Loan-to-Value Limit: Most lenders cap delayed financing at 75% of the home’s value, so you won’t be able to pull out 100% of your cash investment.

- Eligibility Requirements: Lenders will still evaluate your creditworthiness, income, and the property itself before approving the refinance. If you wouldn’t qualify for a mortgage traditionally, delayed financing might not be the right fit.

- Closing Costs: Like any mortgage, refinancing involves costs. Be sure to factor in closing fees and other related expenses when determining if delayed financing makes financial sense for you.

Is Delayed Financing Right for You?

For investors, this strategy offers an additional benefit: it frees up capital for further real estate investments, allowing you to grow your portfolio faster while maintaining control over liquidity.

For more information contact Garrick Werdmuller: https://freshhomeloan.com/schedule-a-meeting

Garrick Werdmuller

garrick@freshhomeloan.com

1151 Harbor Bay Parkway Suite 136

Alameda CA 94502

(510) 282-5456

All loan approvals are conditional and not guaranteed and subject to lender review of all information. Loan is conditionally approved when lender has issued approval in writing, but until all conditions are met, loan cannot be funded. Specified rates and [products may not be available to all borrowers. Rates subject to change according to market conditions and agreed upon lock times set by borrower. Fresh Home Loan Inc. is an Equal Opportunity Mortgage Broker in California. This licensee is performing acts for which a real estate license is required. Fresh Home Loan, Inc. is licensed by the California Department of Real Estate #02137513 NMLS # 2124104

#Mortgage #RealEstateInvesting #PropertyInvestment #DelayedFinancing #CashOutRefinance #RealEstateFinance #InvestorFinancing #FlexibleFinancing #FirstTimeHomeBuyer #RealEstateInvestors #FreshHomeLoan #CaliforniaRealEstate

The post Delayed Financing: What It Is and How It Can Benefit Investors and Homebuyers in General appeared first on Fresh Home Loan.