Carl White's One Page Business Plan for Real Estate Agents

Before We Begin

👉

Download Carl White’s 1-Page Business Plan for Realtors (PDF)

Made for Realtors — useful for

any professional who wants to simplify their business and stay focused.

I know you’re a seasoned professional — and this may feel familiar — but it never hurts to pause, reset, and get intentional.

It’s not about doing more.

It’s about doing the right things, consistently.

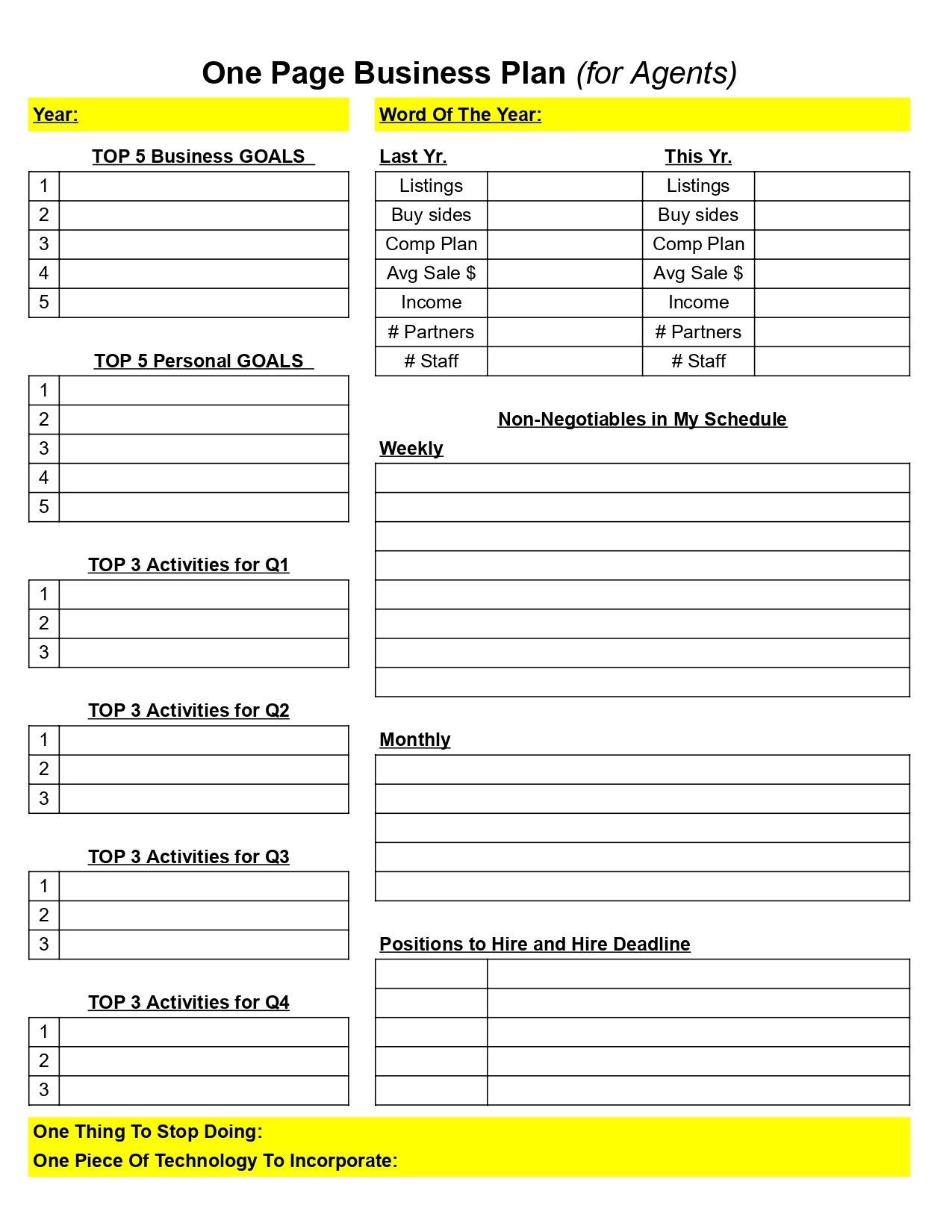

Top 5 Business Goals

Purpose: Define what winning looks like professionally.

What belongs here:

- Closed units

- GCI

- Listings taken

- Buyer sides

- Team growth or leverage

How to explain it:

“If only five business things could go right this year, what would they be?

These should be measurable — not wishes.”

Rule: If it can’t be tracked, it doesn’t go here.

Top 5 Personal Goals

Purpose: Keep life and business aligned.

What belongs here:

- Health

- Family time

- Travel

- Spiritual / mental health

- Lifestyle design

How to frame it:

“Your business exists to support your life — not the other way around.

When personal goals are ignored, burnout always follows.”

This box often creates the biggest “aha.”

Lead Sources

Purpose: Identify where business actually comes from.

Examples:

- Past clients

- SOI

- Open houses

- Online leads

- Agent referrals

How to explain it:

“List the lead sources you will intentionally work — not everything you could do.”

This prevents shiny-object syndrome.

Daily Activities

Purpose: Translate goals into actions.

What belongs here:

- Prospecting calls

- Follow-ups

- Appointments set

- Content creation

- Lead conversion

How to say it:

“Goals don’t close deals.

Daily actions do.”

This box is where discipline lives.

Weekly Activities

Purpose: Create rhythm and structure.

Examples:

- Open houses

- Client check-ins

- Content batching

- Networking events

- Team meetings

Framing line:

“If it’s important, it shows up on the calendar every week.”

Monthly Activities

Purpose: Long-term consistency.

Examples:

- Client events

- Market updates

- Newsletter

- Classes or workshops

- Database cleanup

How to position it:

“This is how you stay top-of-mind without burning out.”

Technology to Implement

Purpose: Support the plan — not complicate it.

Examples listed:

- CRM

- Answering service

- Chat bot

Key talking point:

“Technology should save time or make money.

If it does neither, it doesn’t belong.”

Something to Stop Doing

Purpose: Create space by removing friction.

Examples listed:

- Answering phones

- Email overload

- Working weekends

Power line:

“Growth often starts with subtraction.”

This box is about boundaries and leverage.

Non-Negotiables

Purpose: Lock in standards and identity.

Examples listed:

- Sales calls

- Face-to-face meetings

- Teach a class monthly

- Shoot video weekly

- Post daily on social media

How to explain it:

“These are the actions that happen no matter what — even on bad days.”

This is where consistency beats motivation.

How to Close the Exercise

Use this Carl-White-style wrap:

“This plan isn’t about perfection.

It’s about clarity, focus, and doing the same simple things — every day.”

If you’d like help turning this plan into execution,

strategize with Garrick.

In a focused 15–20-minute conversation, you’ll review your goals and map out a clear strategy using real-world loan programs and tools, including:

- Zero-down FHA & Conventional options to open more buyer conversations

- 5/1 ARMs and payment-strategy programs for affordability and offer strength

- Bank Statement & P&L loans for self-employed clients

- DSCR loans (1–8 units) for investor and rental opportunities

- Bridge, hard money, and fix-and-flip options to win competitive listings

You’ll also cover marketing strategies, open-house and online exposure ideas, and simple lead follow-up systems that convert interest into appointments and contracts.

No pressure. No sales pitch.

Just a clear strategy designed to help you win more deals.

👉

Strategize with Garrick:

https://api.leadconnectorhq.com/widget/bookings/meetwithgarrickhere

Garrick Werdmuller

President & CEO | Mortgage Broker

Fresh Home Loan Inc.

DRE 01368202 | NMLS 242952

Office: 510-282-5456

Email: garrick@freshhomeloan.com

Website: www.FreshHomeLoan.com

All loan approvals are conditional and not guaranteed and subject to lender review of all information. Loan is conditionally approved when lender has issued approval in writing, but until all conditions are met, loan cannot be funded. Specified rates and [products may not be available to all borrowers. Rates subject to change according to market conditions and agreed upon lock times set by borrower. Fresh Home Loan Inc. is an Equal Opportunity Mortgage Broker in California. This licensee is performing acts for which a real estate license is required. Fresh Home Loan, Inc. is licensed by the California Department of Real Estate #02137513 NMLS # 2124104