Fresh Home Loan Releases Realtor® Home Buyers Down Payment Cheat Sheet

As seller credits return to negotiations and buyers become more payment-conscious, understanding down payment structure is becoming just as important as purchase price.

Fresh Home Loan Inc., led by independent mortgage broker Garrick Werdmuller (DRE 01368202 | NMLS 242952), has released its Realtor® Home Buyers Down Payment Cheat Sheet — a structured comparison guide outlining minimum down payments, maximum seller credits, and strategic use cases across today’s most utilized mortgage programs.

In today’s market, offer structure is often outperforming aggressive pricing.

Education is becoming a competitive advantage.

Why This Matters

Agents are navigating:

- Increased use of seller credits

- Payment-sensitive buyers

- Growing demand for zero and low down payment options

- Expansion of non-traditional income borrowers

- Strategic use of adjustable-rate products

Down payment strategy is no longer a footnote in the conversation.

It is a primary negotiation tool.

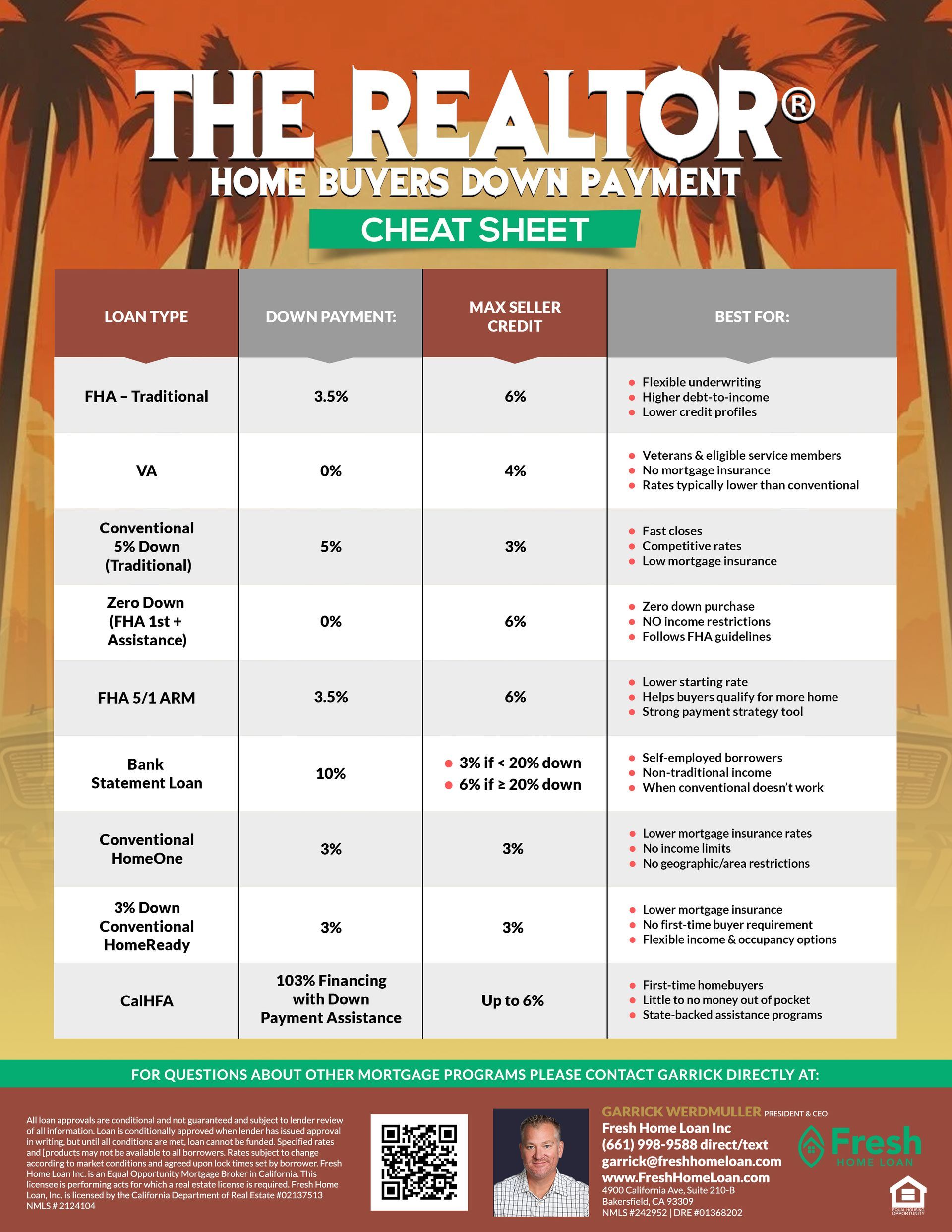

Programs Included in the Cheat Sheet

FHA – Traditional

- 3.5% minimum down

- Up to 6% seller credit

- Flexible underwriting

- Higher allowable debt-to-income ratios

- Useful for moderate credit profiles

VA

- 0% down

- Up to 4% seller concessions

- No monthly mortgage insurance

- Typically strong rate positioning

- Designed for eligible veterans and service members

Conventional – 5% Down

- 5% minimum down

- Up to 3% seller credit

- Competitive rate structures

- Lower mortgage insurance compared to FHA

- Strong for well-qualified buyers

Zero Down (FHA First + Assistance Structure)

- 0% down through assistance layering

- Up to 6% seller credit

- Follows FHA underwriting guidelines

- Designed to reduce out-of-pocket entry

FHA 5/1 ARM

- 3.5% down

- Up to 6% seller credit

- Lower starting rate

- Payment strategy tool for qualification flexibility

Bank Statement Loans

- Typically 10% down

- Seller credit limits vary by structure

- Designed for self-employed borrowers

- Income based on bank deposits rather than tax returns

Conventional 3% Down Options (HomeOne / HomeReady)

- 3% down

- Up to 3% seller credit

- Reduced mortgage insurance structures

- Expanded income flexibility

CalHFA Programs

- Down payment assistance options available

- State-backed assistance structures

- Designed for eligible first-time buyers

Strategic Takeaway

Purchase price gets attention.

Payment structure wins negotiations.

Understanding how down payment percentages interact with seller credits can:

- Improve affordability

- Strengthen offers

- Protect buyer liquidity

- Increase approval confidence

- Create cleaner contracts

The Realtor® Home Buyers Down Payment Cheat Sheet was built to simplify that structure into a single, usable reference page.

For a copy of the cheat sheet or to discuss how to structure your next offer strategically:

Garrick Werdmuller

President & CEO

Fresh Home Loan Inc.

(510) 282-5456

garrick@freshhomeloan.com

#FreshHomeLoan #Realtor #HomeBuyers #HomeFinancing #FirstTimeHomeBuyer #LoanPrograms #SellerCredits #ZeroDownPayment #HomeOwnership #RealEstateMarket #MortgageTips #HomeLoanExperts #CaliforniaRealEstate