Before You Buy a Home, Understand This About Your Credit Score

In today’s digital landscape, many consumers monitor their credit using popular apps and online tools. While these platforms provide useful insights, they can also create a false sense of confidence when preparing for a home purchase.

The reality is simple:

There is no single, universal credit score.

Instead, there are multiple scoring models, each designed for a specific type of lending decision. Understanding this distinction is critical for both homebuyers and real estate professionals.

Different Industries Use Different Credit Models

Credit is evaluated differently depending on the type of financing being considered.

- Auto lenders prioritize performance on installment-based auto loans

- Credit card issuers emphasize revolving credit behavior and utilization

- Mortgage lenders focus on long-term repayment patterns and financial consistency

As a result, a consumer’s credit score can vary significantly depending on which model is used.

For example, a consumer may see a 720 score through a credit monitoring app, while their mortgage-specific score may be closer to 680.

This discrepancy is not an error—it reflects the use of a different scoring model.

Mortgage Credit Scoring Is More Conservative

In mortgage lending, underwriting relies on established FICO models, including:

- FICO 2 (Experian)

- FICO 4 (TransUnion)

- FICO 5 (Equifax)

These models are intentionally more conservative in their evaluation. They tend to:

- Place greater emphasis on payment history

- Respond more negatively to collections or derogatory events

- Focus on long-term credit behavior rather than short-term improvements

This approach reflects the nature of mortgage financing, which typically involves long-term repayment over 15 to 30 years.

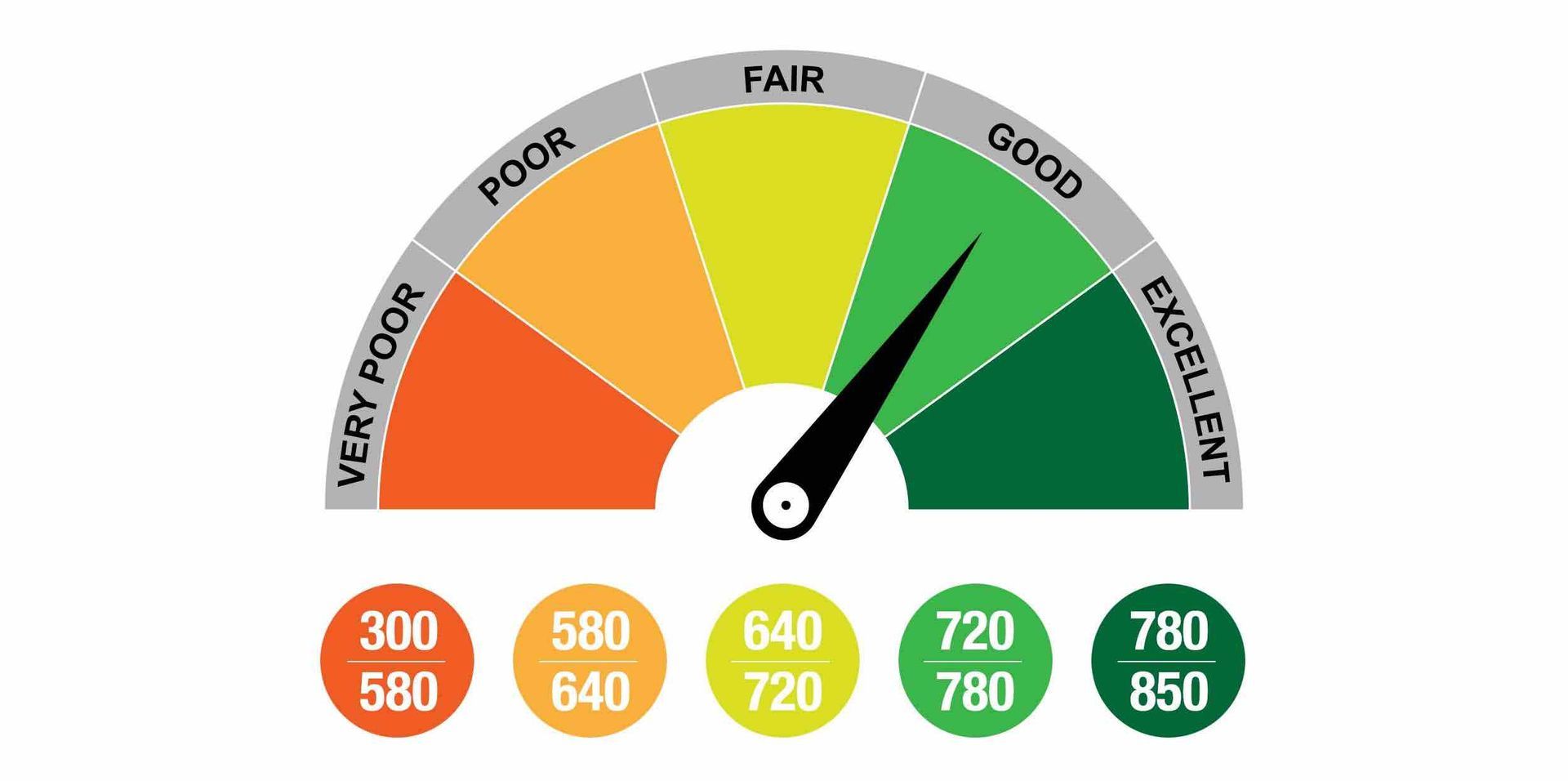

Key Factors That Influence Credit Scores

According to FICO, credit scores are generally calculated based on the following factors:

- Payment history (35%)

- Amounts owed (30%)

- Length of credit history (15%)

- New credit activity (10%)

- Credit mix (10%)

These components collectively determine how a borrower is evaluated from a risk perspective.

How Credit Scores Improve Over Time

Also, according to FICO, credit profiles tend to strengthen when borrowers demonstrate consistent and responsible behavior, including:

- Making all payments on time

- Maintaining low credit utilization (ideally below 30%, with optimal performance below 10%)

- Limiting new credit inquiries and account openings

- Preserving established credit lines to maintain history

These actions contribute to a more stable and favorable credit profile over time.

Implications for Homebuyers

Understanding the distinction between consumer-facing credit scores and mortgage-specific scores is essential during the homebuying process.

A borrower who appears well-qualified based on a general credit score may encounter different results during mortgage underwriting.

This can directly impact:

- Interest rate eligibility

- Loan program qualification

- Down payment requirements

- Overall monthly housing expense

Even small variations in credit score can translate into meaningful differences in long-term cost.

Conclusion

Credit should not be viewed as a single number, but rather as a dynamic profile evaluated differently depending on the lending context.

For homebuyers, the key is not simply achieving a “good” score, but understanding how their credit profile aligns with mortgage-specific requirements—and how it can be strategically positioned to support a successful home purchase.

About Fresh Home Loan

Fresh Home Loan specializes in helping clients navigate the complexities of mortgage financing through strategic planning, education, and access to a wide range of lending solutions.

For more information or a personalized credit and financing review, please visit: https://www.freshhomeloan.com/contact-us

Garrick Werdmuller

President & CEO

Fresh Home Loan Inc.

(510) 282-5456

garrick@freshhomeloan.com

www.FreshHomeLoan.com

All loan approvals are conditional and not guaranteed and subject to lender review of all information. Loan is conditionally approved when the lender has issued approval in writing, but until all conditions are met, loan cannot be funded. Specified rates and [products may not be available to all borrowers. Rates subject to change according to market conditions and agreed upon lock times set by the borrower. Fresh Home Loan Inc. is an Equal Opportunity Mortgage Broker in California. This licensee is performing acts for which a real estate license is required. Fresh Home Loan, Inc. is licensed by the California Department of Real Estate #02137513 NMLS #2124104

#FreshHomeLoan #MortgageTips #CreditScore #FirstTimeHomeBuyer #HomeBuyingTips #MortgageEducation #Realtor #RealEstateAgent #HomeFinancing #PreApproval