HELOC vs Credit Card: Which Is Better for Homeowners?

When homeowners need access to cash, one of the most common questions is:

"Should I use a HELOC or just put it on a credit card?"

The answer depends on your goals, but for larger expenses, a HELOC can often provide significant advantages over traditional credit cards.

Let's take a closer look.

What Do HELOCs and Credit Cards Have in Common?

At first glance, a HELOC and a credit card are surprisingly similar.

Both:

- Provide revolving access to funds

- Allow you to borrow as needed

- Require minimum monthly payments

- Charge interest on outstanding balances

- Can be reused as balances are repaid

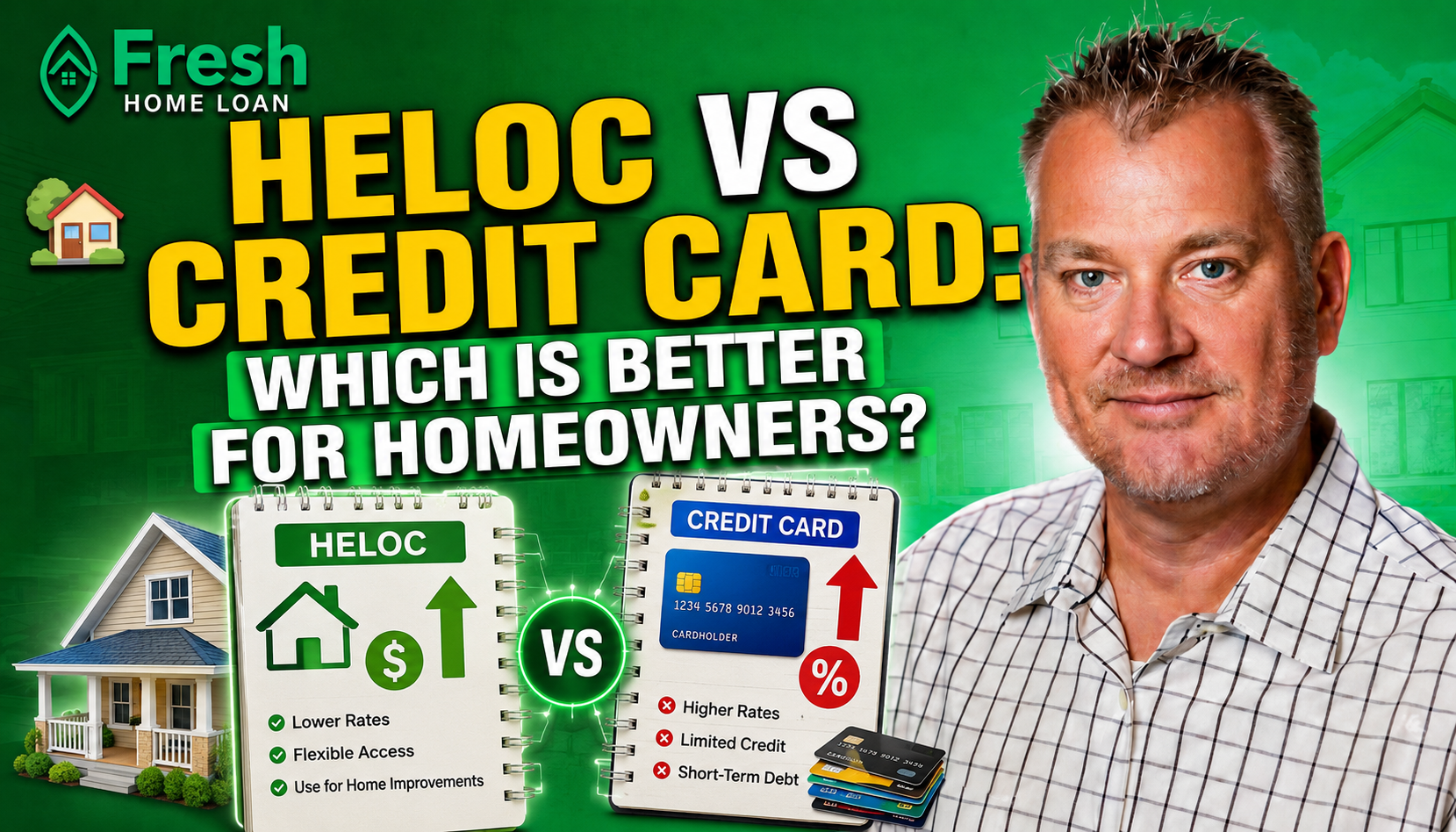

The major difference is what secures the debt.

A credit card is unsecured debt.

A HELOC is secured by the equity in your home.

Because the lender has collateral backing the loan, HELOC interest rates are often substantially lower than credit card rates.

The Interest Rate Difference

Today's credit card rates commonly range from the high teens into the 20%+ range, depending on the card and borrower.

Meanwhile, HELOC rates are typically tied to Prime Rate and often come in significantly lower.

Let's look at a simple example:

$50,000 balance:

- Credit Card at 24% interest

- HELOC at 8% interest

The difference in interest expense can be thousands of dollars per year.

For homeowners carrying substantial credit card balances, this is one reason debt consolidation remains one of the most common uses for a HELOC.

Monthly Payment Flexibility

Like credit cards, many HELOCs offer flexible payment options during the draw period.

Borrowers often have the ability to:

- Make minimum payments

- Pay additional principal

- Pay down and reuse available credit

This flexibility can be extremely useful for homeowners managing large projects or expenses over time.

When a Credit Card May Make More Sense

Credit cards aren't always the bad guy.

For smaller purchases that can be paid off quickly, a credit card may be the better option.

Examples include:

- Travel expenses

- Everyday purchases

- Business expenses paid off monthly

- Rewards and cashback opportunities

If you pay the balance in full every month, a credit card can provide convenience and rewards without accumulating interest charges.

When a HELOC May Make More Sense

A HELOC often shines when the expense is larger or spread over time.

Examples include:

Home Improvements

Kitchen remodels, bathrooms, roofing, windows, landscaping, and major renovations.

ADU Construction

Many California homeowners use HELOCs to help fund garage conversions, detached units, and income-producing ADUs.

Debt Consolidation

Replacing multiple high-interest credit card payments with a single lower-interest payment.

Emergency Reserves

Some homeowners establish a HELOC before they need it, creating access to funds for future opportunities or unexpected expenses.

The Risk Factor

There is an important distinction to remember.

Credit card debt is unsecured.

A HELOC is secured by your home.

That means homeowners should approach a HELOC strategically and responsibly.

The goal is not simply to move debt around. The goal is to use home equity to improve your financial position, increase property value, or accomplish meaningful financial objectives.

Which Is Better?

For short-term spending that is paid off quickly, a credit card may be perfectly appropriate.

For larger expenses, home improvements, ADUs, or consolidating high-interest debt, a HELOC often provides a lower-cost financing solution.

Many homeowners are surprised to learn they can access equity while keeping their existing first mortgage untouched.

Final Thoughts from Garrick

I don't view a HELOC and a credit card as competitors as much as different tools for different jobs.

If you're putting groceries, gas, or a weekend getaway on a credit card and paying it off every month, that's one thing. Get the points!!!

If you're financing a $40,000 kitchen remodel, building an ADU, or carrying high-interest revolving debt, it may be worth exploring whether a HELOC can accomplish the same goal at a significantly lower borrowing cost.

The key is understanding your options and choosing the right tool for the job.

To schedule an appointment with Garrick Weredmuller, President and CEO of Fresh Home Loan Inc, visit:

https://freshhomeloan.com/schedule-a-meeting/

Garrick Werdmuller

President CEO

Fresh Home Loan Inc

510.282.5456 call/text

NMLS 242952

You may also enjoy:

HELOC vs. HELOAN: Unlocking Your Home's Equity Without Touching Your First Mortgage

Understanding the Difference Between a HELOC and a HELOAN

https://www.freshhomeloan.com/understanding-the-difference-between-a-heloc-and-a-heloan

How Does a HELOC Work?

https://www.freshhomeloan.com/how-does-a-heloc-work

Socials:

https://www.facebook.com/freshhomeloan/

https://www.instagram.com/garrickwerdmuller/

https://www.linkedin.com/in/garrick-werdmuller-b044253/

https://www.youtube.com/@FreshHomeLoan

https://www.tiktok.com/@freshhomeloan

#HELOC #HomeEquity #CreditCards #HomeownerTips #MortgageBroker #PersonalFinance #HomeFinancing #FirstTimeHomeBuyer #Realtor #FreshHomeLoan #RealEstate #WealthBuilding #MortgageAdvice #HomeImprovement #FinancialFreedom

All loan approvals are conditional and not guaranteed and subject to lender review of all information. Loan is conditionally approved when the lender has issued approval in writing, but until all conditions are met, loan cannot be funded. Specified rates and products may not be available to all borrowers. Rates subject to change according to market conditions and agreed upon lock times set by the borrower. Fresh Home Loan Inc. is an Equal Opportunity Mortgage Broker in California. This licensee is performing acts for which a real estate license is required. Fresh Home Loan, Inc. is licensed by the California Department of Real Estate #02137513 NMLS # 2124104