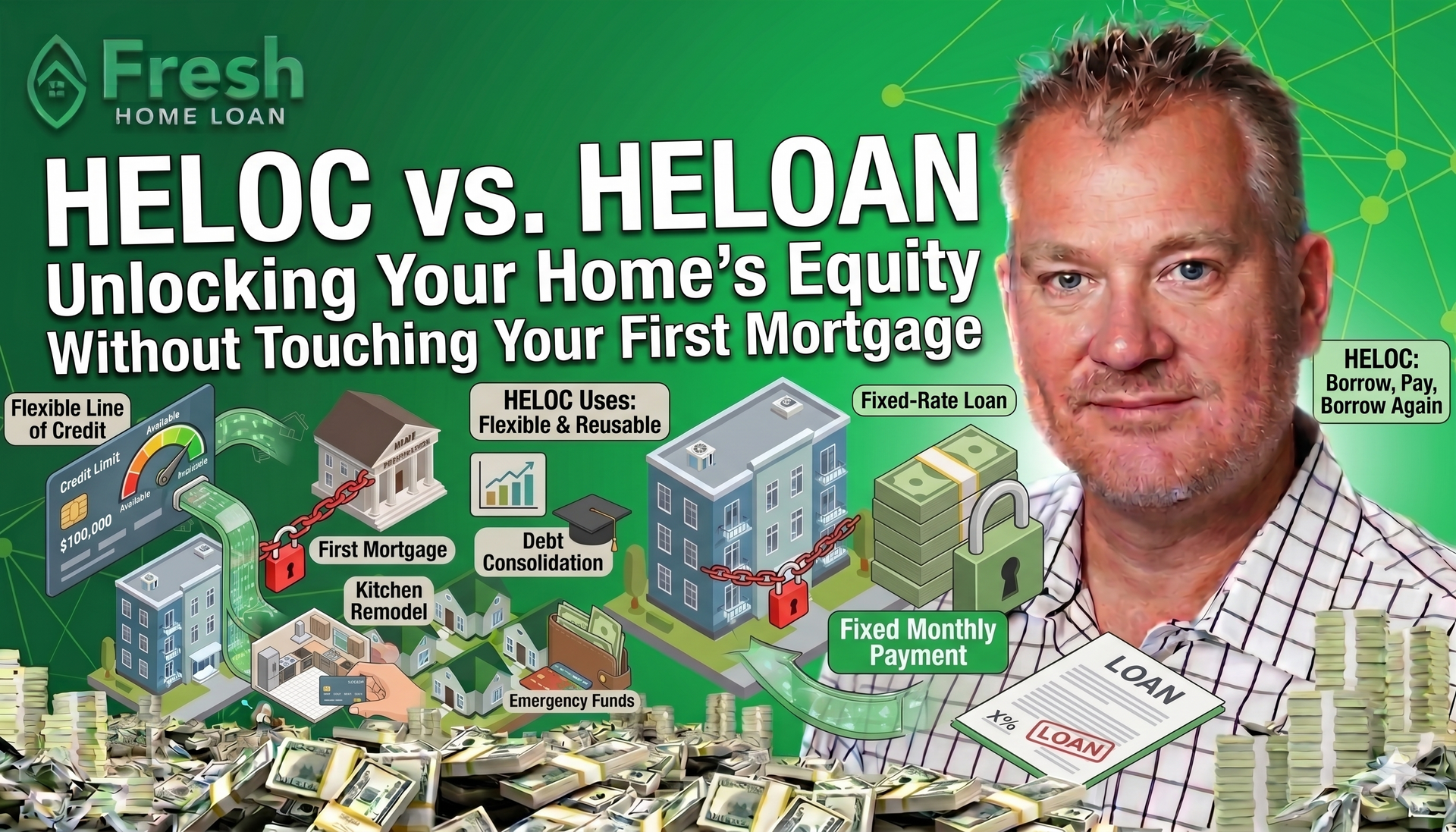

HELOC vs. HELOAN: Unlocking Your Home's Equity Without Touching Your First Mortgage

With many homeowners sitting on low first mortgage interest rates from the past several years, one question comes up again and again:

"Do I really want to refinance my entire mortgage just to access cash?"

In many cases, the answer is no.

That's where a HELOC (Home Equity Line of Credit) or HELOAN (Home Equity Loan) can be a powerful solution.

How Does a HELOC or HELOAN Work?

A HELOC or HELOAN is a second mortgage that sits behind your existing first mortgage.

The important thing to understand is:

Your First Mortgage Does Not Change

If you currently have a mortgage at 3%, 4%, or 5%, that loan remains exactly the same.

Your:

- Interest rate stays the same

- Payment stays the same

- Loan term stays the same

The HELOC or HELOAN is simply added behind the first mortgage, allowing you to access a portion of your home's available equity.

Instead of refinancing your entire loan balance, you're only borrowing the additional funds you need.

HELOC vs. HELOAN: What's the Difference?

HELOC (Home Equity Line of Credit)

A HELOC works similarly to a credit line or credit card.

You are approved for a maximum amount and can draw funds as needed.

Benefits include:

- Flexible access to funds

- Borrow only what you need

- Interest is generally charged only on the amount used

- Great for projects completed over time

HELOAN (Home Equity Loan)

A HELOAN provides a lump sum of money upfront.

Benefits include:

- Fixed loan amount

- Predictable monthly payments

- Ideal for one-time expenses

- Easier budgeting

Common Uses for a HELOC or HELOAN

1. Home Improvements

One of the most popular uses for home equity financing is improving the home you already own.

Examples include:

- Kitchen remodels

- Bathroom renovations

- Roof replacement

- New windows

- Flooring upgrades

- Landscaping

Many homeowners use equity to improve their home's comfort, functionality, and value while keeping their low first mortgage rate intact.

2. Building an ADU (Accessory Dwelling Unit)

ADUs continue to grow in popularity throughout California.

Homeowners are using HELOCs and HELOANs to finance:

- Detached backyard units

- Garage conversions

- In-law suites

- Rental units

An ADU can create:

- Additional rental income

- Housing for family members

- Increased property value

Using home equity is often one of the most affordable ways to fund construction costs.

3. Debt Consolidation

Many homeowners carry higher-interest debt such as:

- Credit cards

- Personal loans

- Medical bills

- Other consumer debt

A HELOC or HELOAN may allow those balances to be consolidated into a single monthly payment.

Potential benefits include:

- Lower monthly payments

- Simplified finances

- Reduced overall interest costs

- Improved cash flow

Every situation is different, but for many homeowners this can be a valuable financial strategy.

Is a HELOC or HELOAN Right for You?

If you have built equity in your home and want access to cash without disturbing your existing first mortgage, a HELOC or HELOAN may be worth exploring.

Whether you're planning a remodel, building an ADU, consolidating debt, or simply creating financial flexibility, there are more options available today than many homeowners realize.

At Fresh Home Loan, we can review your current mortgage, available equity, and goals to help determine which option makes the most sense for your situation.

Final Thoughts…

One of the biggest misconceptions I hear is that homeowners think they need to refinance their entire mortgage to access equity. In reality, many homeowners can keep their current low-rate first mortgage exactly where it is and add a HELOC or HELOAN behind it.

If you have questions about your home's equity or would like to explore your options, let's talk. We serve homeowners throughout the Bay Area, Central California, and beyond.

To schedule an appointment with Garrick Werdmuller, President and CEO of Fresh Home Loan Inc, visit:

https://freshhomeloan.com/schedule-a-meeting/

Garrick Werdmuller

President CEO

Fresh Home Loan Inc

510.282.5456 call/text

NMLS 242952

You may also enjoy:

HELOC vs Credit Card: Which Is Better for Homeowners?

https://www.freshhomeloan.com/heloc-vs-credit-card-which-is-better-for-homeowners

Understanding the Difference Between a HELOC and a HELOAN

https://www.freshhomeloan.com/understanding-the-difference-between-a-heloc-and-a-heloan

How Does a HELOC Work?

https://www.freshhomeloan.com/how-does-a-heloc-work

Socials:

https://www.facebook.com/freshhomeloan/

https://www.instagram.com/garrickwerdmuller/

https://www.linkedin.com/in/garrick-werdmuller-b044253/

https://www.youtube.com/@FreshHomeLoan

https://www.tiktok.com/@freshhomeloan

#HELOC #HomeEquity #HELOAN #CreditCards #HomeownerTips #MortgageBroker #PersonalFinance #HomeFinancing #FirstTimeHomeBuyer #Realtor #FreshHomeLoan #RealEstate #WealthBuilding #MortgageAdvice #HomeImprovement #FinancialFreedom

All loan approvals are conditional and not guaranteed and subject to lender review of all information. Loan is conditionally approved when the lender has issued approval in writing, but until all conditions are met, loan cannot be funded. Specified rates and products may not be available to all borrowers. Rates subject to change according to market conditions and agreed upon lock times set by the borrower. Fresh Home Loan Inc. is an Equal Opportunity Mortgage Broker in California. This licensee is performing acts for which a real estate license is required. Fresh Home Loan, Inc. is licensed by the California Department of Real Estate #02137513 NMLS # 2124104